When keeping tabs on their investments, obligations, and assets, businesses might use any number of company accounting methods. To estimate how quickly its assets will lose value, a company might look at its cumulative depreciation. Having this knowledge may be crucial in determining how to best allocate assets or invest in the future.

In this post, we will discuss what cumulative depreciation is, as well as explore three different methods for calculating it and present examples.

What is Cumulative Depreciation?

The sum amount of a company’s depreciation expenditures is known as accumulated depreciation. Any and all expenses related to an asset’s depreciation, from the moment it is first used until the end of its useful life, are included in the cumulative depreciation.

Since the value of an asset declines as it ages, cumulative depreciation plays a role in how companies determine where to put their money. Over time, assets might depreciate due to reasons including outdated technology, regular usage, and general wear and tear.

What is The Significance of Depreciation Over Time?

Monthly, quarterly or annual accounting periods are used by businesses to keep track of depreciation costs and see how they impact income over time. These depreciation costs accrue over time to form the cumulative depreciation balances at the start of each accounting period.

Profits or losses on the sale or retirement of an asset may be calculated with the help of accumulated depreciation. Gain or loss from the sale of an asset is subject to taxation, and this amount must be reduced by the asset’s cumulative depreciation. Capital assets of a firm may consist of:

- Vehicles with Company Equipment

- Furniture

- Fixtures

- Machinery

- Buildings

- Property

Methods for Determining The Amount of Accumulated Depreciation

The straight-line technique, the declining balance method, and the double-declining balance depreciation method are the three primary approaches how to calculate accumulated depreciation. An explanation of each follows.

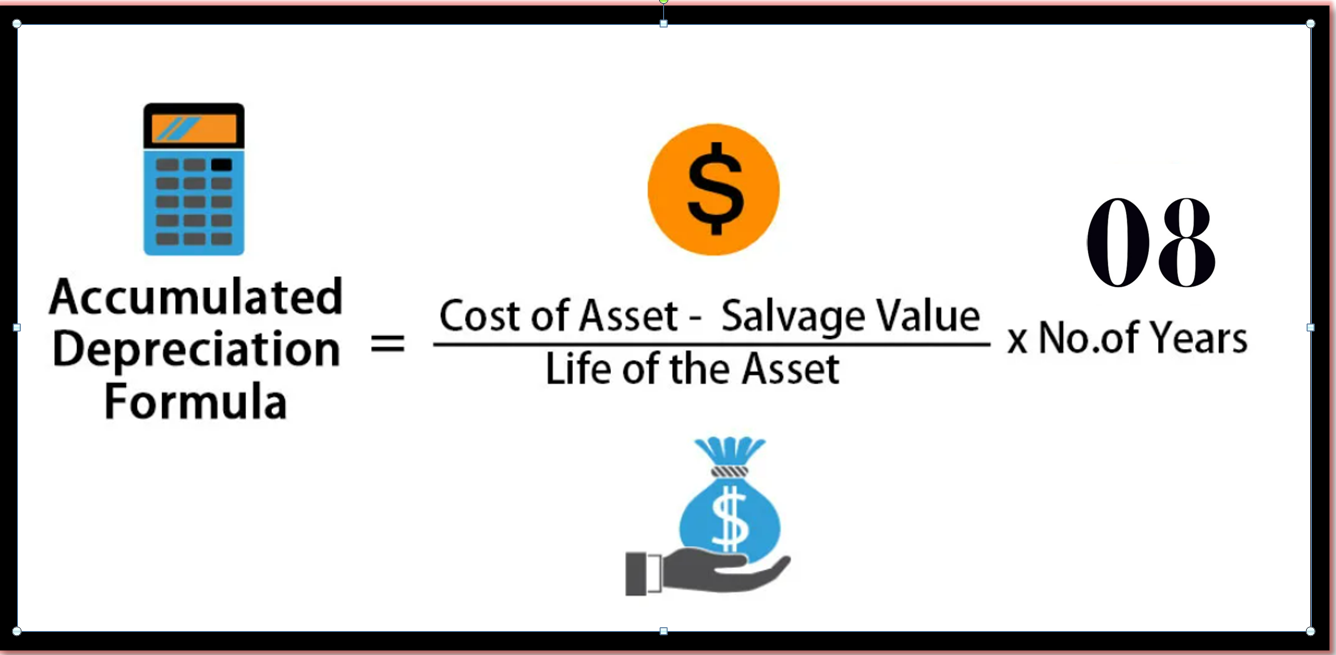

Straight-line Method

Accumulated depreciation is often calculated using the straight-line technique. This procedure’s formula is as follows:

(Cost of Asset less Salvage Value) / Anticipated Service Life

The cost of an asset is its market value at the time it is acquired, whereas its salvage value is its estimated market worth after it is no longer useful. The number of years you anticipate using the asset is the projected years of usage.

Declining Balance Method

You may figure out how much an asset has depreciated over time using the decreasing balance approach, which is an accelerated depreciation methodology. As the falling balanced approach ensures that the majority of an asset’s depreciation is taken into account early in the asset’s useful life, it is an essential tool for maximizing tax benefits.

This indicates that the majority of an asset’s depreciation costs will be incurred in the first few years after the item is acquired. Depreciation is a fall in the value the firm assigns to an asset over time as its usefulness and worth decline.

The following decreasing balance formula may be used to get the total years of depreciation:

An asset’s annual depreciation is calculated by multiplying its depreciation factor by (1 / Asset’s remaining useful life) and its remaining value.

Divide the final figure by 12 to get the monthly amount. Multiply by two if you’d rather use a more extreme rate of depreciation.

Double-declining Balance Depreciation Method

The double-declining balance depreciation technique is an accelerated depreciation approach used in corporate accounting to calculate the cumulative depreciation of an asset, much like the declining balance method.

This form of depreciation in accounting is twice as fast as the traditional decreasing balance approach. When an item is expected to lose a significant portion of its value shortly after purchase or when its useful life is expected to be short, businesses often adopt the double-declining balance depreciation technique to account for the loss in value.

Depreciation Accumulation: How to Figure It Out

Straight-line Method

If you need help figuring out how to calculate accumulated depreciation over time using the straight-line method, here’s a handy guide:

First, We Deduct The Value of The Salvage From The Total Price.

For the straight-line technique of computing cumulative depreciation, knowing the asset’s salvage value is a prerequisite. An asset’s salvage value is the sum you anticipate receiving after it has been retired from service. This is the amount you would get if you were to sell, retire, or scrap an assist at its estimated total worth.

Consider the following scenario: you paid $750 for a computer and think you can get around $75 in scrap value for it. Once the asset’s salvage value has been determined, the initial purchase price may be adjusted downwards. Put these numbers into the formula based on the computer hardware example:

Annual Depreciation = ($750 – $150) / (Expected Useful Lifespan)

Multiply The Difference by The Number of Years of Service.

The entire estimated lifetime of an asset is represented by the number of years of usage in the cumulative depreciation calculation. The estimated value of an asset during its lifespan may be calculated using data tables provided by the Internal Revenue Service. The difference between the salvage value and the cost may be calculated by dividing the sum by the number of years of projected usage.

If we take the same $750 computer as an example and suppose that the IRS has data showing that it was used for a total of six years, we get:

An asset’s annual depreciation is calculated as follows: ($Asset cost – Expected salvage value) / Expected years of usage = ($750 – $75) / (6 + 1) = $675 / 6 = $112.50

Monthly Depreciation is Calculated by Dividing the Yearly Depreciation By 12

Once you have the total depreciation for the year, you may break it down further to see how much was lost in a given month, quarter, or another fiscal period. Using the given figure, we can calculate the monthly cumulative depreciation by dividing the yearly depreciation by 12: $112.50 / 12 = roughly $9.38. Over the course of the asset’s useful life, it will lose $9.38 in value every month in depreciation.

Double-declining Balance Depreciation Method

To get the total amount of depreciation that has accrued, use the double-declining balance depreciation formula and proceed as follows:

Determine The Annual Rate of Straight-line Depreciation

Simply divide one by the number of years you expect the asset to last, and you’ll get your straight-line depreciation rate. Continuing with our earlier example, if the computer has a six-year lifetime, the straight-line depreciation rate would be 1/6, or 0.16. In percentage terms, this works out to 16% of the initial value every year for the duration of the asset’s useful life (multiply by 100 to get the figure).

Determine The Asset’s Book Value If It Has Been Depleted.

The remaining book value of an asset may be determined by using a straight-line depreciation rate calculation. The amount may be determined by subtracting the accrued depreciation from the initial purchase price. Two years after purchase, the computer would have a book value of $590.20 if it depreciated at a rate of 16% per year.

Third, Multiply The Remaining Amount By The Straight-line Rate.

Multiply the straight-line rate by the amount of book value that remains after deducting any discounts. Consider our digital illustration:

Two times the linear depreciation multiplied by the residual value is $94.43. This comes out to a total of $94 in the first example and $160 in the second.

Division By Two

When using the double-declining balance depreciation technique, this sum is multiplied by two: 2 x ($94.43) = $188.86. The formula’s other inputs are held constant. So, the computer asset’s depreciation is $188.86 each year.